Banking led off fintech news again this week with the regional bank "mini crisis" continuing to unfold

While giving a speech the acting head of the OCC stated that banks need more competition not less; he also commented on companies like Amazon or Apple becoming banks, Noreika states; “Laws that prevent companies with resources and means from becoming competitor banks only serve to protect existing big banks from would-be rivals”; as Crowdfund Insider reports the benefits of having big tech companies become banks could help to lower cost, increase access and help to serve those who might be left behind by traditional banks. Source.

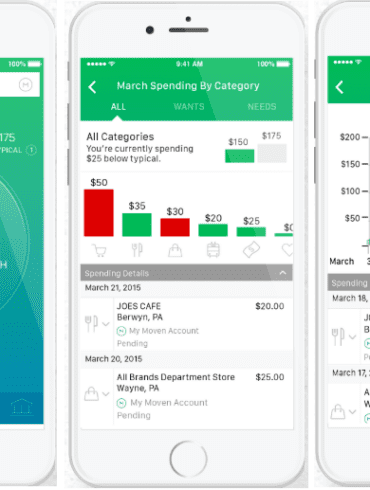

Today we're joined by Brett King, founder and executive chairman of Moven, one of the world's original digital banks, and Lex Sokolin, global head of fintech at ConsenSys. Lex and I discussed Moven's recent announcement to shutter its B2C business on episode 170 of Rebank. And we're happy to have the opportunity to connect with Brett directly to discuss the decision in more detail.

Most significant banks have a mobile app with features that allow individuals to conduct close to their entire banking life on their phones; keeping up with the operating systems from Apple and Google is a challenge for the banks; banks are not as nimble as fintech startups and so there is a lot more detailed of a process to go through when making technology updates; banks have learned that 80% of users update operating systems within the first month of a new release, which puts pressure on the banks to act quickly; talking to American Banker about staying current, Alice Milligan, the chief customer and digital experience officer of Citi's global cards business, said, "This requires us to stay at the cutting edge of device and operating system developments in the industry."; prioritizing what features are most important is key, not everything can get done quickly and this forces banks to make difficult choices; as more people use technology in their financial lives, banks and fintech companies will need to make sure they try to stay ahead of the curve. Source

This week, we look at:

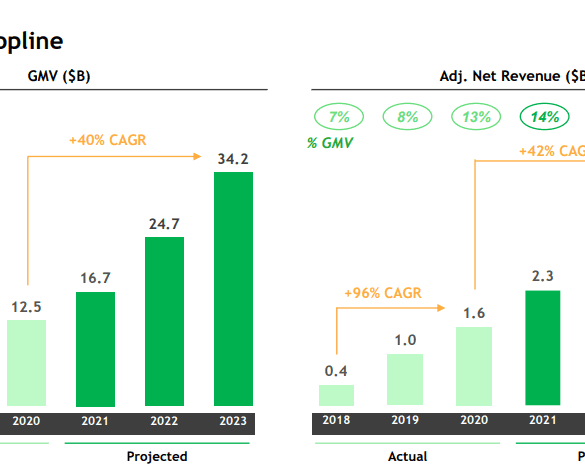

The economics of Southeast Asia’s largest super-app and its $40 billion SPAC valuation

The industrial logic of building out financial features adjacent to the core business of transportation and delivery

Why this model has not worked for Uber, but has worked for Apple, and the broader impact on financial services.

Welcome back to the Fintech Blueprint / Rebank podcast series hosted by Will Beeson and Lex Sokolin. Max Friedrich is a fintech analyst a ARK Invest, a public markets investment manager focused on disruptive technologies including autonomous tech, robotics, fintech, genomics and next generation internet. Max recently published a report on digital wallets, including Venmo and Square’s Cash App, which is available for download on ARK’s website. In this conversation, we explain why Cash App has seen exponential growth.