Financial literacy is a national problem.

According to the Financial Capability Survey, 39% of adults in the UK don’t feel confident managing their money. This can have devastating effects on the economy.

A survey conducted by CBI Economics found that the national debt stemming from adult numeracy failure (a marker for financial literacy) could amount to £20 billion per year in lost output.

Additionally, they found that prioritizing financial education in schools could add almost £7 billion to the economy every year, impacting the rate of business formation and job creation significantly.

As economic conditions worsen, the adverse effects of financial illiteracy will likely cause increased detriment. For Gen Z, the generation just moving into adulthood, increased financial literacy is vital.

“Gen Z is a very interesting one,” said Nikos Melachrinos, CEO of Quirk. “They’re a lot more activated than prior generations. They are actually becoming the most financially savvy generation. But they’re having the biggest macroeconomic wealth-building issues to face. In a way, it’s also out of necessity that they’re becoming financially educated much earlier than the rest.”

The cost of living has increased substantially in the UK over the past few years, with inflation prices as high as in the 1980s. According to the Spring Budget projections of 2022, real household disposable income will fall by 2.2%, the biggest fall in living standards since the 1950s. Salary rate increases have not increased at the same rate as housing prices, and many are turning to alternative forms of wealth creation to make up the deficit.

“I would say they’re the first generation taking things onto their own hands,” he continued.

Social media improves access to information but not necessarily from trusted sources

Social media has opened the world to increased ease of access to information. This brings with it both benefits and challenges. Melachrinos explained that GenZ turning to social media for financial education has meant they are a lot more exposed to advanced forms of wealth creation. At times information may not come from trusted, qualified sources.

“Traditionally, all surveys show that people go to their parents as the first source of learning about money. Versus Gen Z is the first time that that’s flipped; they go online to social media to learn about personal finance. Our research shows around 40% of them first go to social media before asking their parents,” said Melachrinos.

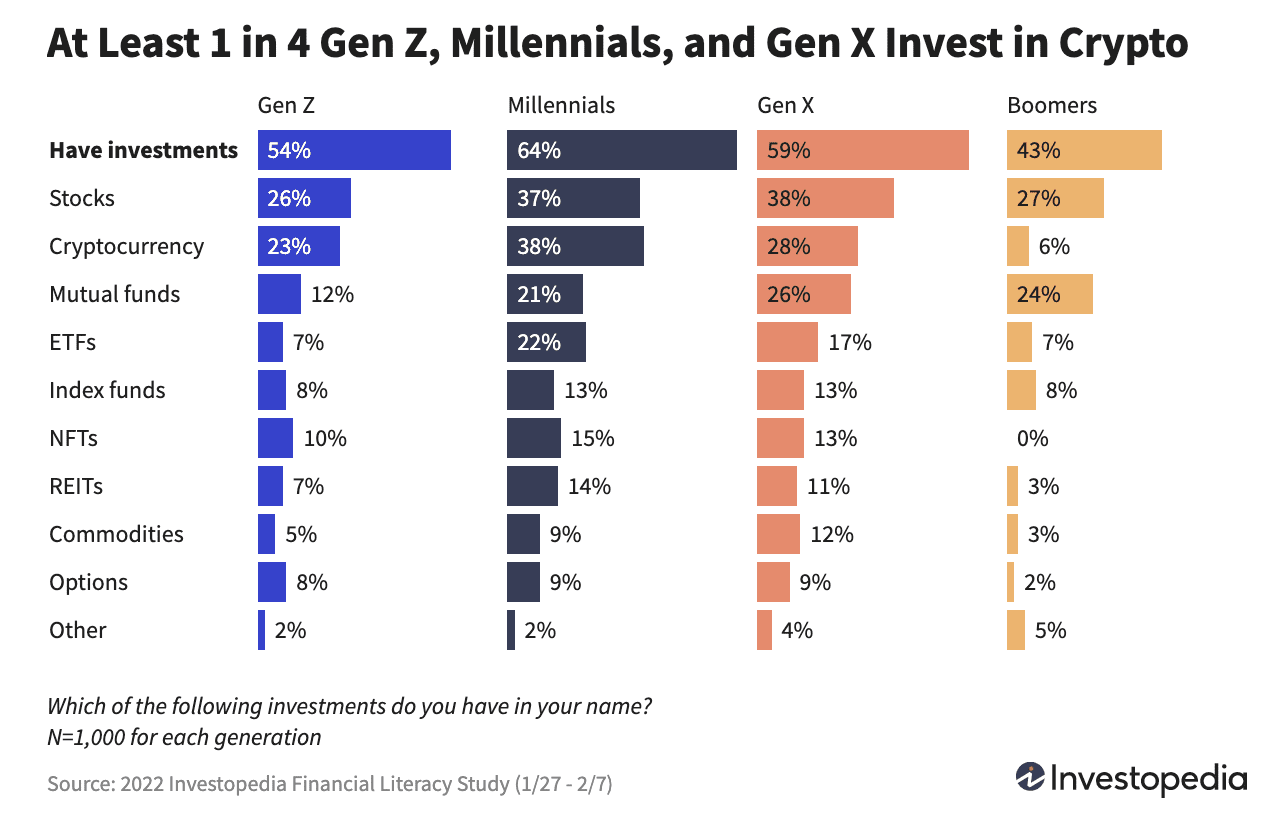

The media hype surrounding digital assets such as NFTs and Cryptocurrencies has had an effect. Investopedia found that 48% of GenZ respondents with investments invest in cryptocurrencies, more than those in GenX and above. Investment in NFTs was also comparatively high.

“You have 18-year-olds, all of a sudden talking about investing in stocks or buying crypto, in a way that prior generations weren’t. What’s tricky is that you have people who are too young to invest in traditional ways because they’re under 18. So they can’t open a brokerage account, but they can engage in crypto. So, a young person is much more likely to first get into crypto than traditional financial products. And that is scary.”

Quirk does the legwork to inform GenZ investment.

The high-risk environment of investment in digital assets is not for the faint-hearted and is particularly dangerous for those with low levels of basic financial literacy.

“We feel a responsibility to bring expert points of view and legitimate content out there. Because there’s a lot of shuffling of cryptocurrencies, for example,” continued Melachrinos.

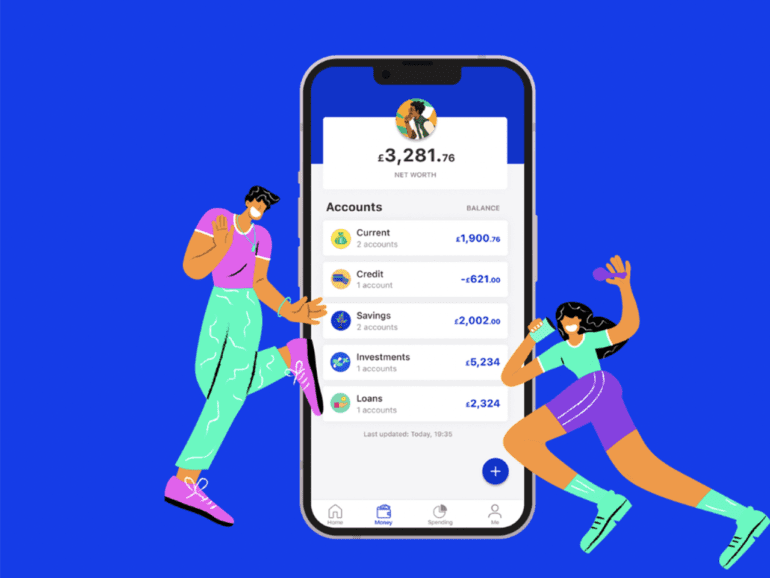

Quirk is a financial literacy app launched this month, targeting the financial literacy of GenZ. To date, users can link accounts and learn about tracking expenditure and managing finances. Tips about basic economic concepts and actionable insights are available to users to help improve their understanding. Gamification is used extensively, encouraging users to work through the subject matter.

“Literacy and education are the bare bones; it’s like the spine. Before we get into product features, let them buy stocks, or engage in crypto-related products, we want to have done the legwork, teaching them about everything. A big part that is lacking is the knowledge to action gap.”

Aside from in-app information, they have made a significant push in their social media strategy. Melachrinos explained that they had gained a lot of engagement through TikTok and Instagram. “Part of the experience follows outside the app as well. We put so much content out there.”

Tailoring experience to match user personality

A significant selling point of the app is in the onboarding process. To access Quirk, users fill out a personality test. Information, language, and suggested actions are then tailored to the user based on the result.

The idea for the personality test came from a Cambridge University study that found that happiness is closely linked to spending in accordance with personality type. The Quirk creators worked closely with the scientist involved in the study to develop the test.

“It’s psychometrically valid and uses well-established measures, like the big five, which is quite common for 16 personalities, a Myers Briggs type thing, but we also combine it with some more money-related questionnaires that exist,” said Melachrinos.

“What we saw, in essence, was that it was a great engagement tool. It’s also a great way to start the conversation around money because there is a lot of anxiety. People sometimes struggle to engage with it. This was a softer, fun way of getting into the money conversation.”

“How risk averse someone is to maybe how impulsive they are, has a big influence on their finances. At the end of the day, money is very linked to lifestyle and personal decisions. It’s not this, strictly financial, mathematical relationship that we have with it, from how we spend it to how we invest.”

New approaches to wealth creation may be on the horizon.

Based on the trends he has seen, Melachrinos believes we are entering a new era of wealth creation with GenZ. With exposure to investment options, and a need to turn to alternative income streams in the face of the increased cost of living, GenZ is likely to approach finances differently than generations before. This makes basic financial literacy critical to avoid bad decisions.

With this in mind, Quirk addresses the essential elements of financial education, attempting to create a firm foundation for users to create wealth. Their humanist approach, focusing on the user’s personality, aims to maximize engagement, despite the distractions of screaming social media headlines announcing the latest NFT millionaire.

“This generation will find other ways of wealth building, reaching financial independence, and retiring. A lot of that involves creating side businesses and finding alternate income streams.”

“Depending on the personality type, how you frame a saving goal, for example, for someone extroverted versus someone who is not, changes. It affects their engagement, how much they save, and spending patterns.”

RELATED