One of the most popular features for readers is my quarterly returns post. I have been sharing the details of my Lending Club and Prosper returns since the 4th quarter of 2011 and I will continue doing so.

While the principle of transparency seems to be less important at the major platforms these days here at Lend Academy we are still very much committed to it. So, every quarter I will share the details of all my P2P lending investments and show you how I am doing.

This past quarter brought several changes to my portfolio. I added two new investment accounts that now brings my total to ten separate investments. I admit this is a little excessive but if you read the details below you will understand why I have added two new accounts. Before we do that, though, let’s get right to the numbers.

Overall P2P Lending Return Now at 11.11%

My overall returns, while still solidly in double digits, continue to slowly decline. The returns for my core six holdings, each one has been open for several years, has dropped below 10% for the first time since I started investing more aggressively. There are two reasons for this: more defaults and lower average interest rates. Both Lending Club and Prosper continue to reduce their interest rates in order to attract more borrowers, so it is becoming more difficult to achieve those 10-12% returns that many of us have become accustomed to for the last several years.

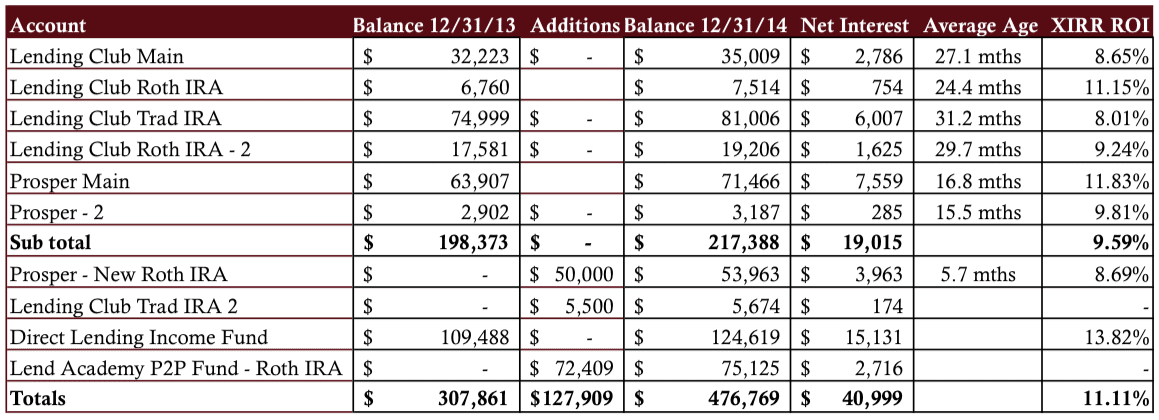

Now on to my numbers. Click the table below to see it at full size.

As you look at the above table you should take note of the following points:

- All the account totals and interest numbers are taken from my monthly statements that I download each month.

- The Net Interest column is the total interest earned plus late fees and recoveries less charge-offs.

- The Average Age column shows how old, on average, the notes are in each portfolio. These numbers are obtained from the platforms.

- The XIRR ROI column shows my real world return for the trailing 12 months (TTM). I believe the XIRR method is the best way to determine your actual return.

- The four new accounts have been separated out to provide a level of continuity with my previous updates.

- I do not take into account the impact of taxes.

- The extended chart showing returns displayed at Prosper and Lending Club as well as my adjusted returns can be viewed here.

Now, let me go through each account in turn, to give you some context to the above table.

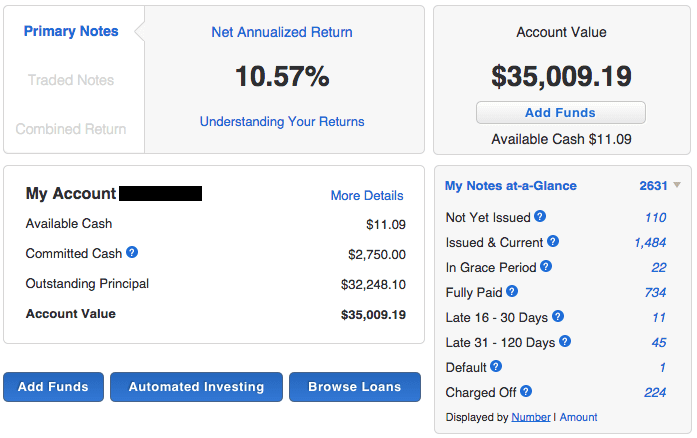

Lending Club Main

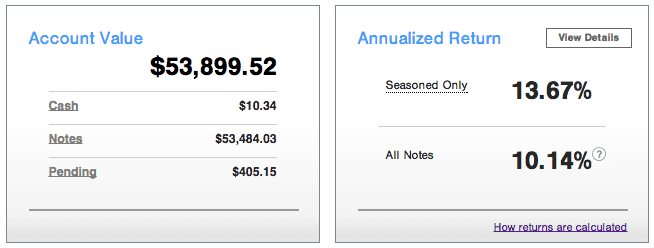

This is the account that started it all. I opened this account back in 2009 with $500. I have added to it several times, an additional $24,000 to be precise, although it has been a couple of years now since I have added anything. And I will not be adding any more, probably ever. This is a taxable account and I am only adding new money to my retirement accounts now.

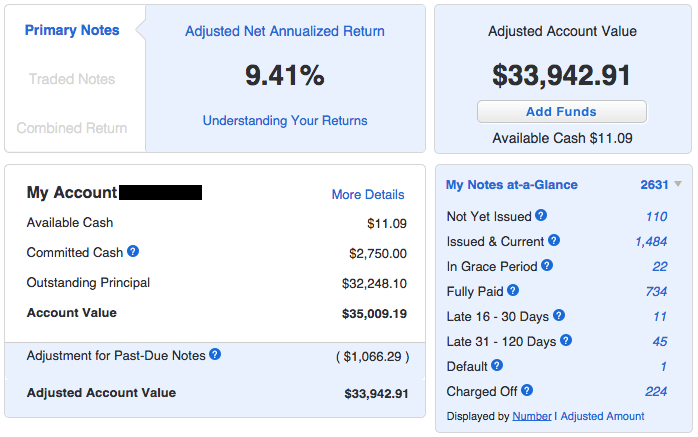

You will see two graphics with this account. I have taken a screenshot of both the standard account screen (above) as well as the screen that shows adjusted returns (below). You can see the difference in the return numbers for both – the adjusted returns looks at all your late loans and adjusts your return accordingly. It is a more accurate way to look at returns. My own actual (XIRR) returns have remained steady when comparing the TTM returns with last quarter’s numbers at 8.65%.

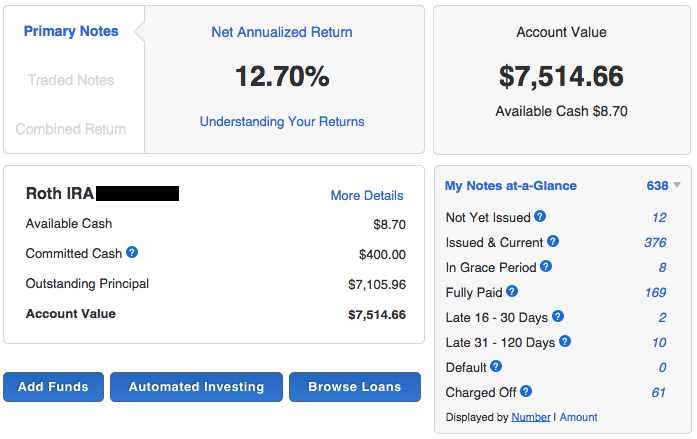

Lending Club Roth IRA

Readers who are paying very close attention will notice something unusual with this account. I added $5,500 back in the 2nd quarter of 2014 but that amount has now disappeared. What happened was this. I always file an extension every year for my taxes and I was unsure when I made this deposit into my Roth IRA back in April whether or not I would be able to keep this because of income limitations. It turns out that in 2013 I made more income than I expected (mainly from my equity investments) so I had to do what is known as a re-characterization.

What this means is that I had to move this money from a Roth IRA to a Traditional IRA. Only problem was that I didn’t have a Traditional IRA at Lending Club. So, in October I opened a new account at Lending Club and moved $5,500 worth of notes from my Roth IRA to my new Traditional IRA (more on that later). What this also meant is that my average age of my portfolio increased sharply as almost all of the newer notes were moved to the new account.

Lending Club Traditional IRA

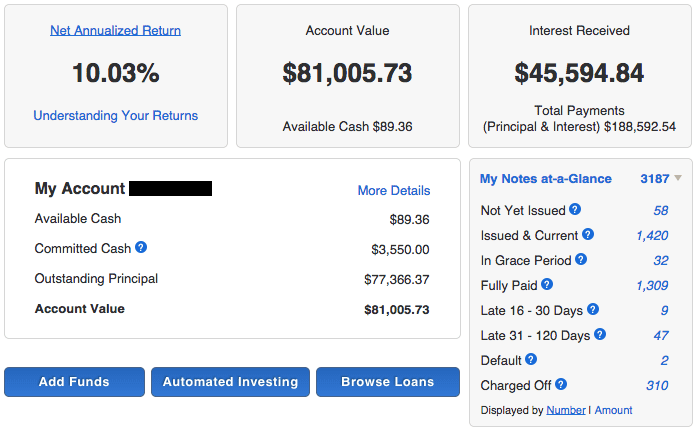

This account is almost five years old now. And yes, I did say I didn’t have a Traditional IRA at Lending Club, which is still true. This IRA is in my wife’s name and it is a combination of many 401(k) and IRA accounts that were rolled over into one Lending Club account back in early 2010. This is my largest account at either Lending Club or Prosper and it had a disappointing quarter. My TTM return went from 9.74% down to 8.01% and my net interest earned dropped from $7,038 to $6,007 – a substantial decrease. My strategy has not changed but the number of defaults has certainly increased – from 272 to 310 in the previous three months. That may sound like a lot but keep in mind the account is almost five years old now and I have 1,420 notes that are issued or current. Regardless, I would like to see an improvement in this account in the 1st quarter.

Lending Club Roth IRA – 2

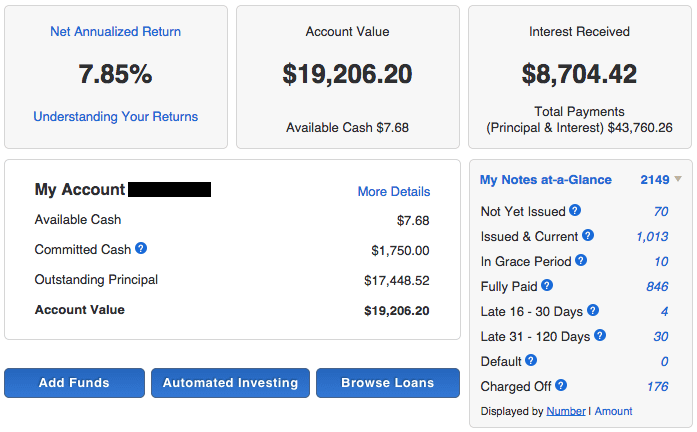

By contrast, this account is doing much better as the TTM return continues to rise. I migrated to a more aggressive approach with this account about 18 months ago and the returns have reflected that. My TTM return bottomed out at 4.91% in Q4 of 2012 and has now increased to 9.24% and is now my second best Lending Club account. Now, I should point out that even though the average note age is around 30 months the higher interest notes in this account are still relatively young. So, my return here could continue to increase before defaults start to bite. I am using Lending Club’s automated investing process with this account using my Super Simple filter.

Prosper Main

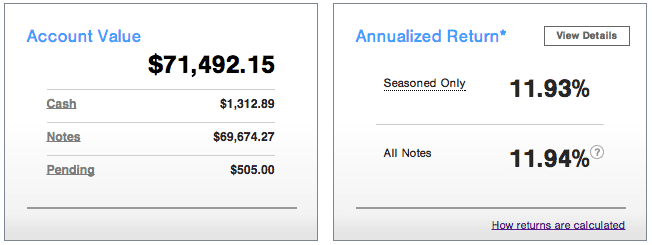

Now over four years old this account continues to be my strongest performer. This taxable account has had exactly $50,000 in deposits since inception so I am now approaching a 50% increase in value. While my TTM return did dip slightly from last quarter it is still a very healthy 11.83% return.

Prosper – 2

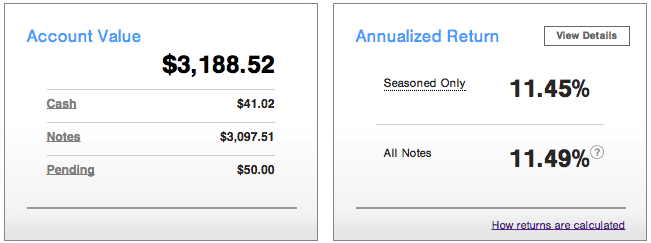

This account has always been something of an experiment. From day one (almost 4 years ago) I have focused solely on E & HR loans. Since I started producing these quarterly reports this account has been the most volatile. Returns have ranged from a high of 23.56% to a low of 4.93% just last quarter. In just three months the return has more than doubled. This is what happens when you have a minimally diversified portfolio focused on the highest risk loans.

Prosper – Roth IRA

I opened this account almost a year ago with a slightly different intention. All of my other P2P lending accounts have been invested aggressively in higher risk loans, so I wanted this new account to take a more conservative approach. I rolled over $50,000 from a Roth IRA account and I have my own firm, Lend Academy Investments, manage this account with our balanced portfolio. It invests primarily in A, B and C grade loans at Prosper using our own models.

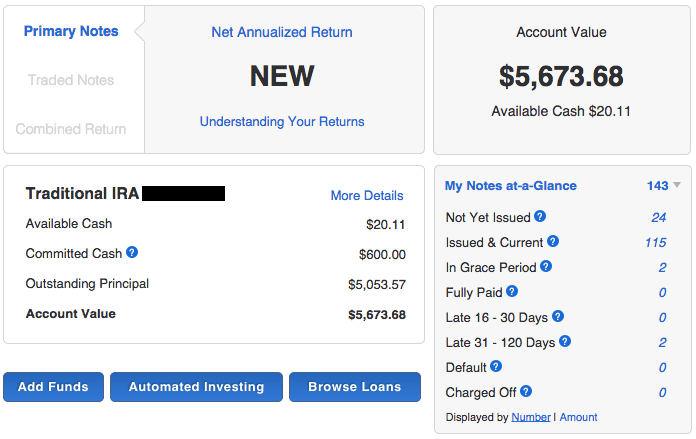

Lending Club Traditional IRA – 2

As I said above in the Lending Club Roth IRA section I opened this account out of necessity. I needed to do a recharacterization of my Roth IRA. What I didn’t say above is that Lending Club makes this process very easy. This all happened very quickly and I just had to download my notes and select $5,500 worth of notes and they moved them over to this new account. And because this account is so new it does not have an official return yet.

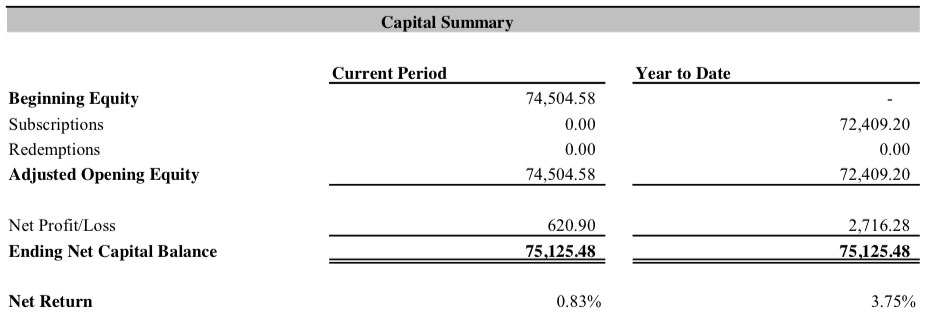

Direct Lending Income Fund

The Direct Lending Income fund continues to be the best performing investment in my entire portfolio. It is the main reason why I am still able to maintain double-digit returns. Being a fund this is a completely passive investment – the fund manager, Brendan Ross, does all the work in selecting loans. The focus of this fund is in short term high yield small business loans through a variety of online platforms.

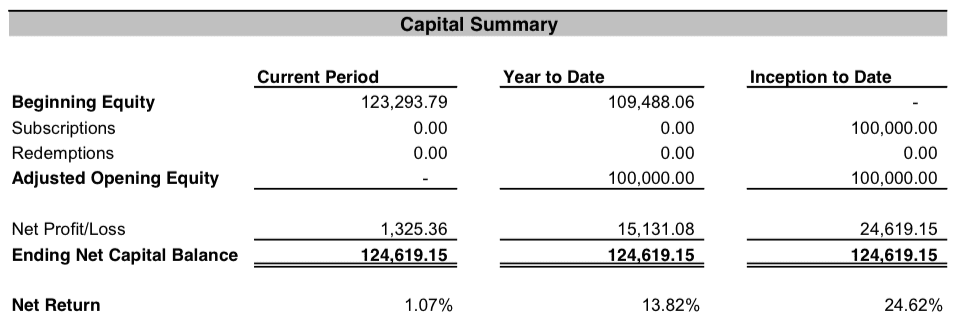

Lend Academy P2P Fund – Roth IRA

This is my other account that is new with this report. Lend Academy Investments, offers a private fund for accredited investors and late last year I rolled over part of my Roth IRA into this fund. It invests in the loans issued by Lending Club, Prosper and Funding Circle with a small position in Upstart as well. Our target return with this fund is 10% net to investors after fees and while it is still early days we are exceeding that goal. And unlike your portfolios at Lending Club and Prosper the fund values every loan at fair value at the end of every month, writing down the value of any late loans. We use our own proprietary credit model to invest in this fund.

Final Thoughts

With my core accounts dipping below 10% for the first time in two and a half years I can’t say I am delighted with these returns. I do believe it is more difficult to earn 10-12% returns than it used to be as I said above. I know some of you have urged me to juice my returns by selling loans on the secondary markets but I want to keep my investments passive. I want to show others that you can earn a good return without having to monitor your account on a daily basis. So, while I am a little disappointed in the decline I think overall I am still quite happy with these investments.

At the end of every quarterly update I like to highlight one number: Net Interest earned. This is the money that shows the actual gains in your account (before taxes). I always like to see this number grow because eventually, when I retire some day, I want to live off the interest generated by these investments. As I continue to add to my investments I expect this number to keep growing – it now stands at $40,999 interest earned in 2014.

I am always happy to hear what you think – please share your thoughts in the comments section below.