For four years now I have been sharing the quarterly returns of my P2P lending investments here. I get emails from so many people who like this feature of the blog so I know it is one of the most popular parts of Lend Academy. Needless to say I am committed to continuing this practice.

There has been some talk in recent months both in the media and on the forum about an increase in defaults. Ryan covered this topic well earlier this week so I won’t dwell on it here. Suffice it to say that there is some evidence that defaults have increased slightly in the second half of last year and those increases are more pronounced in the higher risk loans. This also happens to be where my portfolio is concentrated and as you will see my returns have been impacted.

So, let’s get right to the numbers.

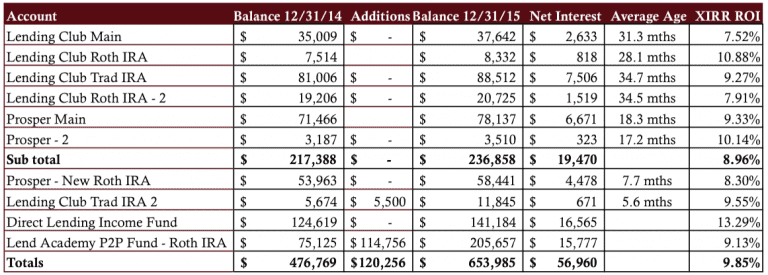

Overall P2P Lending Return Now at 9.85%

For the first time since 2012 (when my account had a more conservative mix) my overall returns have dropped below 10%. My trailing twelve month return ending December 31, 2015 stood at 9,85% a decline of almost 1% from three months ago. The returns for my core six holdings, each one has been open for several years, has dropped to 8.96%.

Throughout 2015 both Lending Club and Prosper reduced their interest rates, with that trend only reversing in the past couple of months. I am very curious to see if this increase will have a material impact on returns going forward or if it will be offset by a future rise in defaults. Suffice it to say the days of easy 10-12% returns that many of us have enjoyed will become more difficult.

Now on to my numbers. Click the table below to see it at full size.

As you look at the above table you should take note of the following points:

- All the account totals and interest numbers are taken from my monthly statements that I download each month.

- The Net Interest column is the total interest earned plus late fees and recoveries less charge-offs.

- The Average Rate column shows the weighted average interest rate taken directly from Lending Club or Prosper.

- The XIRR ROI column shows my real world return for the trailing 12 months (TTM). I believe the XIRR method is the best way to determine your actual return.

- The four newer accounts have been separated out to provide a level of continuity with my previous updates.

- I do not take into account the impact of taxes.

- The extended chart showing returns displayed at Prosper and Lending Club as well as my adjusted returns can be viewed here.

Now, let me go through each account in turn, to give you some context to the above table.

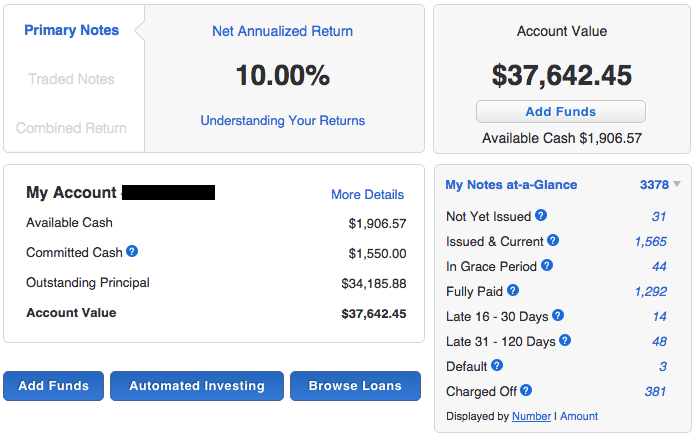

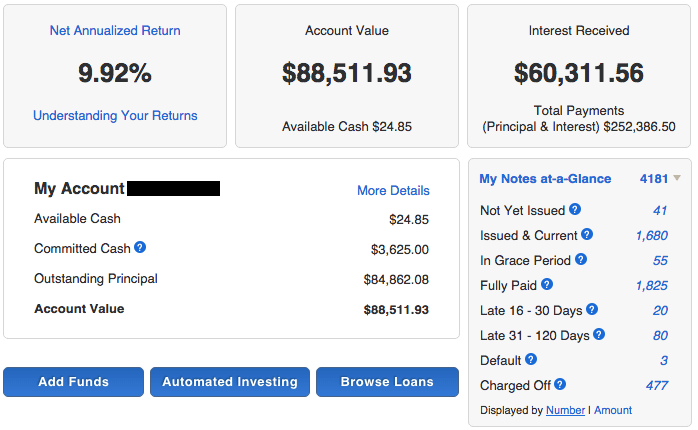

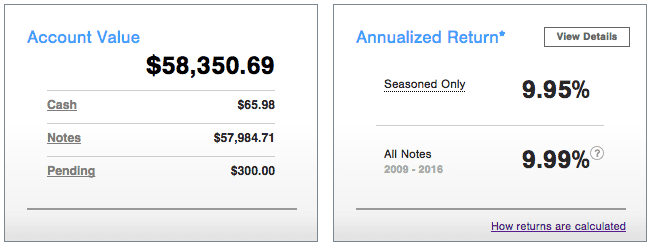

Lending Club Main

This is the account that started it all. I opened this account back in June of 2009 with $500. I have added to it several times, an additional $24,000 to be precise, although it has been several years now since I have added any new money here. This is a taxable account and my policy is to only add new money in my retirement accounts now.

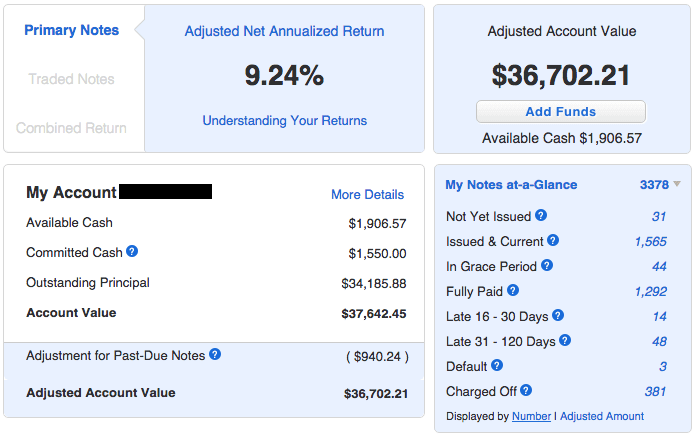

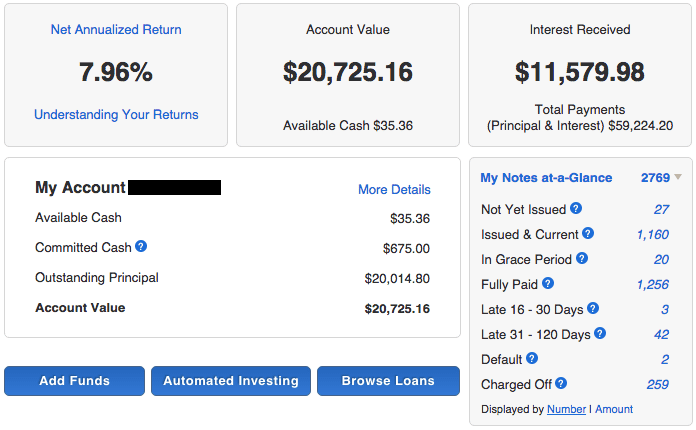

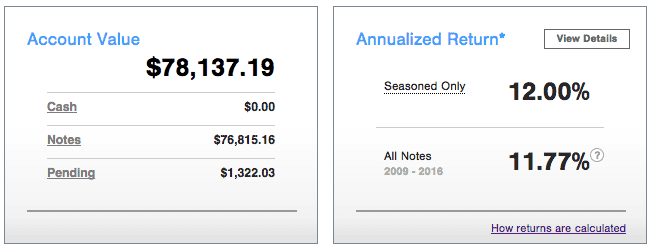

You will see two graphics with this account. I have taken a screenshot of both the standard account screen (above) as well as the screen that shows adjusted returns (below). You can see the difference in the return numbers for both – the adjusted returns looks at all your late loans and reduces your return based on future expected defaults. You will see the account value as well as the annualized return are adjusted downwards. I think this is a more accurate way to look at returns.

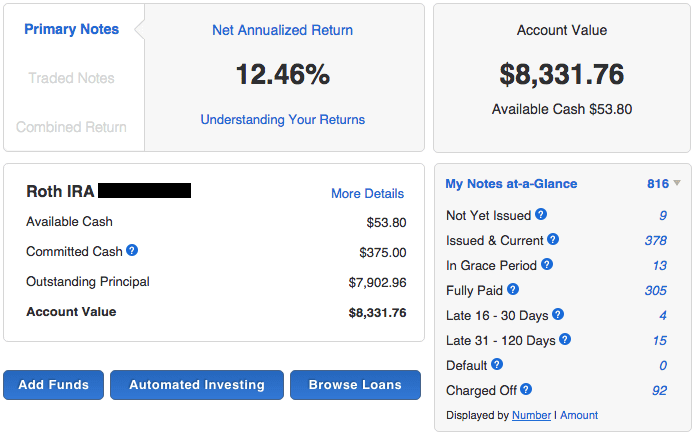

Lending Club Roth IRA

While only a small account my Roth IRA has always been one of my favorites. It has been one of my best performing Lending Club accounts for many years – one of the advantages of a small account is that you can get very targeted with your filters and so only choose a tiny proportion of Lending Club’s platform. For the last several years my strategy with this account has been based on my Filter 1 in this post.

Lending Club Traditional IRA

This account is almost six years old now. This is my largest account at either Lending Club or Prosper and it seems to have settled into a consistent 9-10% return now. I like the fact that this account just passed a quarter of a million dollars in repayments of both principal and interest since I opened it back in 2010 by rolling over my wife’s old 401(k).

Lending Club Roth IRA – 2

This account used to be the most conservative in my portfolio. It was originally setup as a Lending Club PRIME account in 2010 and I let Lending Club manage my investments for me investing only in B- and C- grade accounts. I still let Lending Club invest automatically in this account but I now do so using my Super Simple filter which is more aggressive. My returns have increased from a low of below 5% to almost 8% today.

Prosper Main

Now five years old my first Prosper account continues to be a strong performer. After starting with just $1,000 this taxable account has had exactly $50,000 in deposits since inception so I have now surpassed a 50% increase in value. My XIRR return has remained steady from a quarter ago at 9.35%.

Prosper – 2

This account is my fun account I have created as an experiment. From day one (almost 5 years ago) I have focused solely on E & HR loans, the very riskiest of all loans on Prosper. Because it is such a small account investing in the highest risk loans returns have been volatile – ranging from a high of 23.56% to a low of 4.93% in 2014. Less than 18 months since that low the return has more than doubled. This is what can happen when you have a minimally diversified portfolio focused on high risk loans.

Prosper – Roth IRA

I opened this account back in 2014 with a slightly different intention. All of my other P2P lending accounts have been invested aggressively in higher risk loans, so I wanted this new account to take a more conservative approach. I rolled over $50,000 from a Roth IRA account and I have our sister company, NSR Invest, manage this account with our balanced portfolio. It invests primarily in A, B and C grade loans at Prosper using proprietary credit models.

Lending Club Traditional IRA – 2

This account was open out of necessity. I needed to do a recharacterization of my Roth IRA because my income ended up being higher than expected and I no longer qualified to contribute to a Roth IRA. Since I had already made my contribution to the Roth IRA I had to get these loans moved to a new Traditional IRA. Lending Club made this process very easy as they transferred loans that were held in my Roth to this Traditional IRA. This account is just over a year old and therefore still has a relatively high NAR.

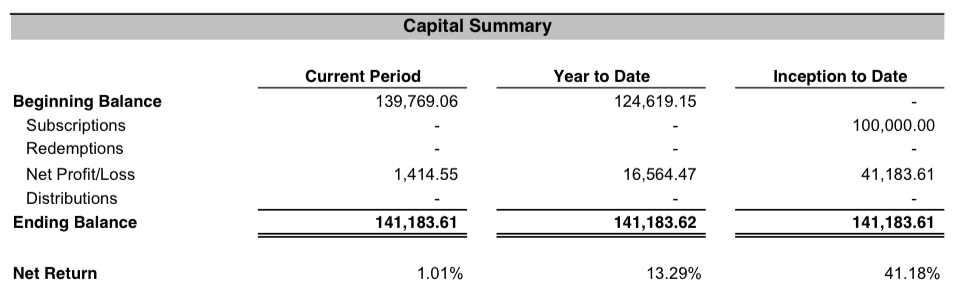

Direct Lending Income Fund

But for my investment in the Direct Lending Income fund my overall returns would be far worse. It continues to be the best performing investment in my entire P2P lending portfolio. Being a fund this is a completely passive investment – the fund manager, Brendan Ross, does all the work in selecting loans. The focus of this fund is in short term, high yield small business loans through a variety of online platforms.

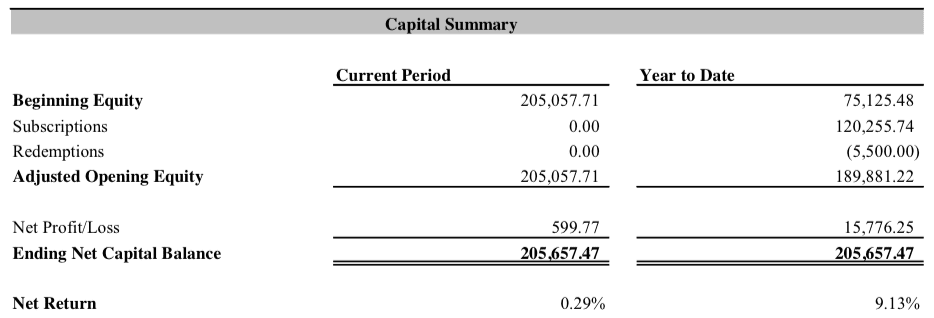

Lend Academy P2P Fund – Roth IRA

This is my other fund account. This one is managed by NSR Invest and it is a private fund for accredited investors. Late last year I rolled over a large part of my Roth IRA into this fund. It invests in the loans issued by Lending Club, Prosper and Funding Circle with a small position in Upstart as well. The net return was much lower in December than it has been historically and here is the explanation from the CEO of NSR Invest, Bo Brustkern:

The Lend Academy fund’s NAV reflected the change in rates at Lending Club and Prosper when each of these origination platforms raised rates, in the month it occurred. That means an immediate price adjustment is recognized, which is very different from what happens for a fund using the typical Loan Loss Reserve methodology, which nearly all other funds in our industry are using. Funds that use Fair Value are attempting to deliver a more accurate NAV, which naturally means a more “fair” NAV for investors entering and exiting a fund.

Final Thoughts

It seems we have entered a new normal. No longer are 10-12% returns easy to achieve – I think the new normal is 8-10% for sophisticated investors. And for those people who look at their Lending Club or Prosper returns and see double digits I encourage you to compare that number with the XIRR method and see the difference. I only have one Lending Club and Prosper account that shows a return of less than 9.9% but in reality my TTM return is only 8.96%.

At the end of every quarterly update I like to highlight one number: Net Interest earned. This is the money that shows the actual gains in your account (before taxes). I always like to see this number grow because eventually, when I retire some day, I want to live off the interest generated by these investments. As I continue to add to my investments I expect this number to keep growing – it now stands at a healthy $56,960 for interest earned in 2015.

I am always happy to hear what you think and answer your questions – please share your thoughts in the comments section below.