One the founding tenets of P2P lending was transparency. As the industry has matured this tenet has been watered down somewhat but here at Lend Academy we are still 100% committed to it. Which is why every quarter I bring you my quarterly returns post. I have been sharing the details of my Lending Club and Prosper returns for many years and I will keep doing so.

I have continued to add new money into my P2P lending portfolio and this quarter I rolled over a good part of my IRA into the Lend Academy P2P Fund. I now have ten different accounts, which I admit is a lot, but with taxable, Traditional IRA and Roth IRA in both my name and my wife’s name, spread across two platforms, I have found this number to be necessary.

I will go through each one of these ten accounts below and provide you with a screenshot as well as a little explanation of each one. But first, let’s get right to the numbers.

Overall P2P Lending Return Now at 11.34%

This past quarter saw a slight rise in my overall return from 11.11% to 11.34%. One the other hand, the returns for my core six holdings (each one has been open for several years) continues to decline slowly going from 9.59% in Q4 2014 to 9.29% in Q1 2015. While I continue to suffer from a large number of defaults the situation is exacerbated by the decline in interest rates at both Lending Club and Prosper. For this reason, I am now sharing the weighted average interest rate of each investment (where available) so everyone can clearly see how this is tracking.

Now on to my numbers. Click the table below to see it at full size.

As you look at the above table you should take note of the following points:

- All the account totals and interest numbers are taken from my monthly statements that I download each month.

- The Net Interest column is the total interest earned plus late fees and recoveries less charge-offs.

- The Average Rate column shows the weighted average interest rate taken directly from Lending Club or Prosper.

- The XIRR ROI column shows my real world return for the trailing 12 months (TTM). I believe the XIRR method is the best way to determine your actual return.

- The four new accounts have been separated out to provide a level of continuity with my previous updates.

- I do not take into account the impact of taxes.

- The extended chart showing returns displayed at Prosper and Lending Club as well as my adjusted returns can be viewed here.

Now, let me go through each account in turn, to give you some context to the above table.

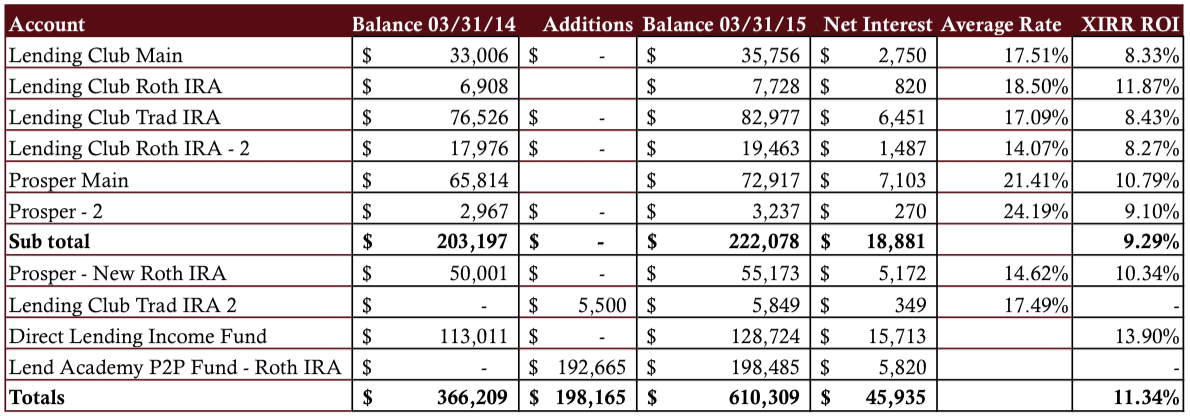

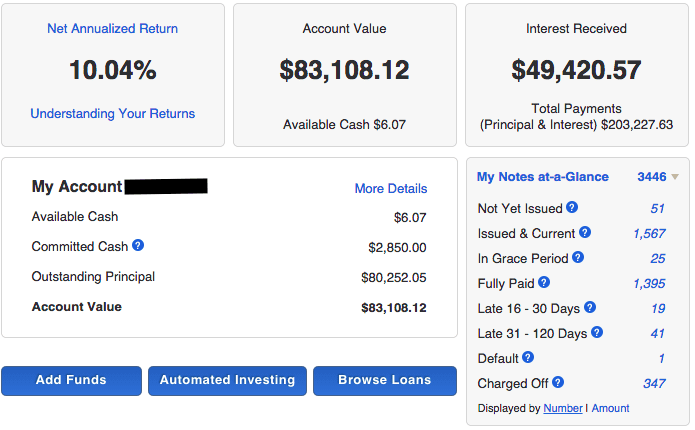

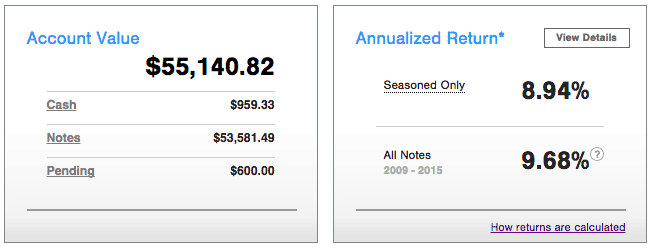

Lending Club Main

This was my first account that has now been open for almost six years. It has gone through several different strategies over the years. I started off in a conservative way like many investors but gradually transitioned to a more aggressive approach. This is a taxable account and I will not be adding to it again – as we explain here a retirement account is the best way to invest in this asset class.

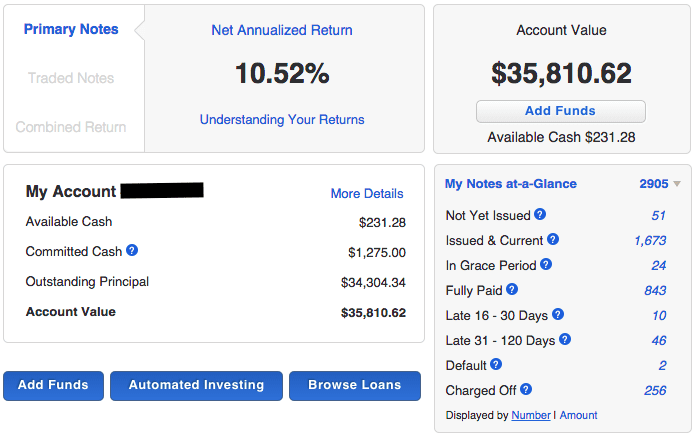

You will see two graphics with this account. I have taken a screenshot of both the standard account screen (above) as well as the screen that shows adjusted returns (below). You can see the difference in the return numbers for both – the adjusted returns looks at all your late loans and adjusts your return accordingly. It is a more accurate way to look at returns particularly for newer accounts.

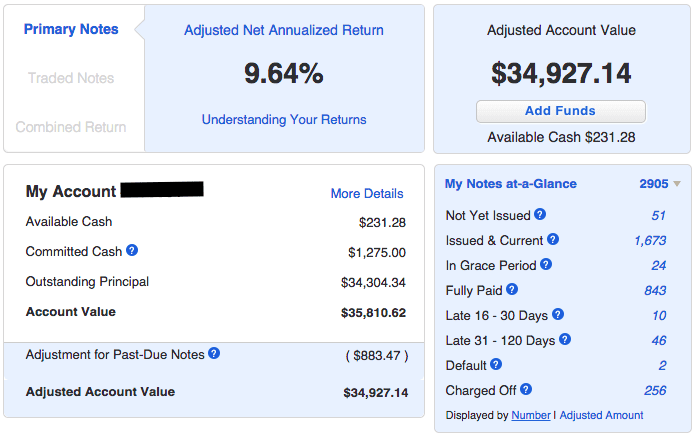

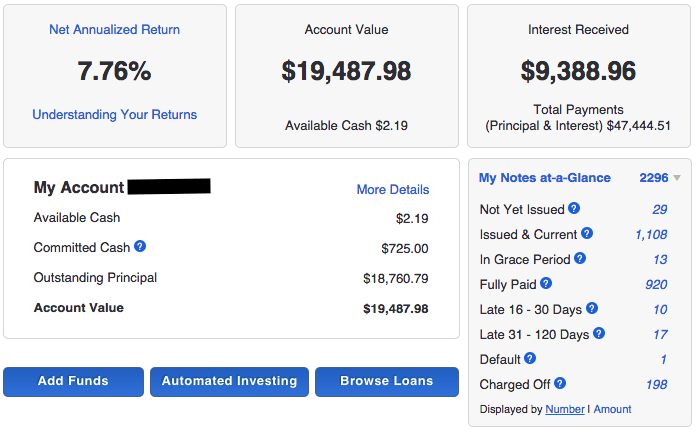

Lending Club Roth IRA

This Roth IRA account just celebrated its fourth birthday. This is my most aggressive Lending Club account with the highest average interest rate. I have only invested in loan grades D-G pretty much from day one so this continues to be my best performing Lending Club account. While the economy keeps chugging along the way it has I expect this account will continue to do well. After dipping below 10% for a couple of quarters last year my real return on this account is now back solidly in double digits.

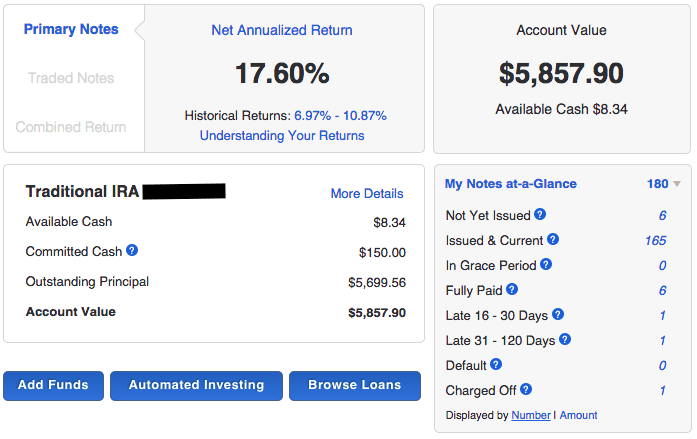

Lending Club Traditional IRA

This is my wife’s Traditional IRA and it is also my largest account at either Lending Club or Prosper. I opened this account in April 2010 by rolling over several 401(k)’s and IRA accounts that my wife had accumulated over the years. After many quarters of declines it was good to see the returns for this account reverse direction, they increased from 8.01% to 8.43% in the previous quarter.

Lending Club Roth IRA – 2

This account used to be my most conservative in my portfolio. It was originally setup as a Lending Club PRIME account in 2010 and I let Lending Club manage my investments for me investing only in B- and C- grade accounts. I still let Lending Club invest automatically in this account but I now do so using my Super Simple filter.

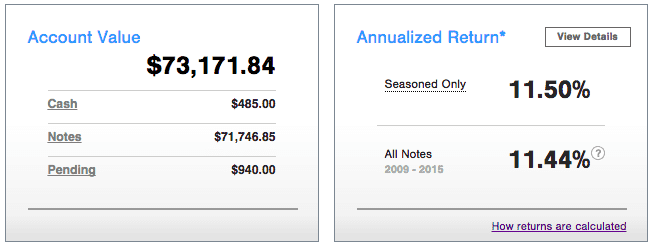

Prosper Main

Switching over to Prosper, we see my original Prosper taxable account. I opened this account in 2010 and eventually invested $50,000 after slowly adding to it over a several year period. This has been my most consistently high performing account, always providing double digit returns since inception. Although my 10.79% real return in Q1 marks the lowest return ever for this account.

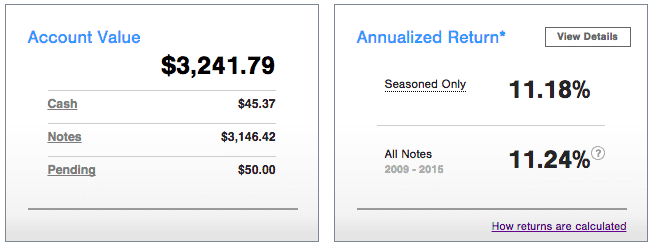

Prosper – 2

This is my most volatile and least diversified account. It has always been something of an experiment for me as I like to see what happens when you only have 100 notes or so invested. And I have only invested in the most aggressive notes as you can see by my 24.19% weighted average interest rate. What happens in an account like this is that defaults have an outsized impact. Just six months ago real returns on this account were under 5%, today they are back over 9%.

Prosper – Roth IRA

I opened this account a little over a year ago with a slightly different intention. All of my other P2P lending accounts have been invested aggressively in higher risk loans, so I wanted this new account to take a more conservative approach. I rolled over $50,000 from a Roth IRA account and I have my own firm, NSR Invest (formerly Lend Academy Investments), manage this account with our balanced portfolio. It invests primarily in A, B and C grade loans at Prosper using our own models.

Lending Club Traditional IRA – 2

This account was opened out of necessity. I needed to do a re-characterization of my Roth IRA because of income limitations. I had to move $5,500 from my Roth IRA to a Traditional IRA, a process that Lending Club made very easy. This is a new account and like all new accounts the Net Annualized Return number that Lending Club provides is pretty meaningless. I like that Lending Club includes the Historical Returns range on new accounts now – that gives a much more accurate picture. I expect my long term returns here will fit somewhere within that range.

Direct Lending Income Fund

I am still a big fan of the Direct Lending Income fund mainly because it continues to be the best performing investment in my entire portfolio. It has been over two years now since I opened this account and the returns have been very consistent. I think Brendan Ross, the fund manager, has done an excellent job on delivering on his promise to investors and this is one of the success stories of this industry. The focus of this fund is in short term high yield small business loans through a variety of online platforms.

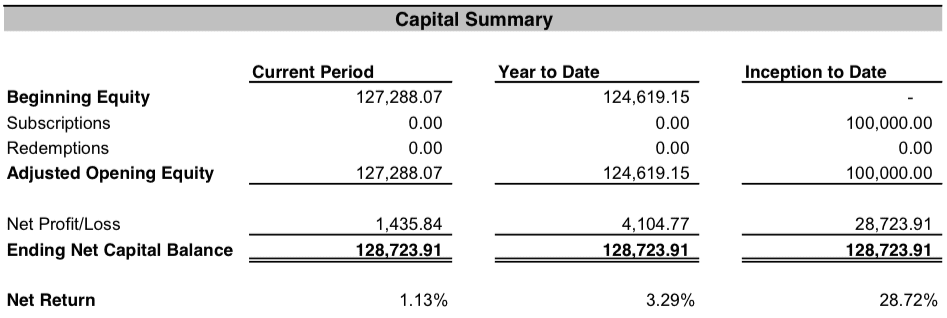

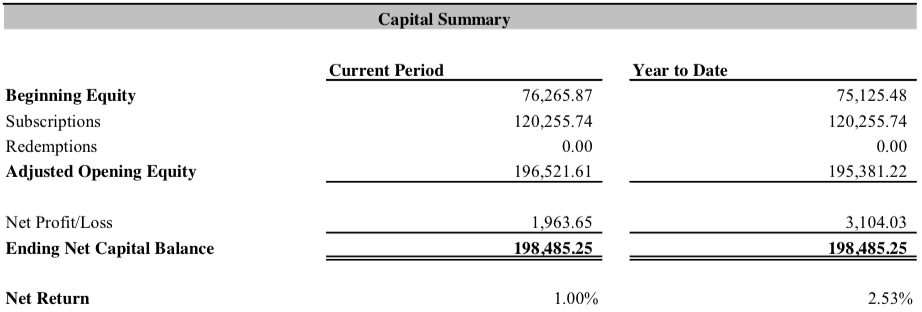

Lend Academy P2P Fund – Roth IRA

You may remember that last month my investment management firm Lend Academy Investments merged with NickelSteamroller to create NSR Invest. We offer a private fund for accredited investors and late last year I rolled over part of my Roth IRA into this fund. In March, I rolled over another part of this Roth IRA so I now have almost $200,000 invested in our fund. It invests in the loans issued by Lending Club, Prosper and Funding Circle with a small position in Upstart as well. Unlike your portfolios at Lending Club and Prosper these kinds of funds value every loan at fair value at the end of every month, writing down the value of any late loans.

Final Thoughts

As I said last quarter I think it is more difficult to earn 10-12% returns than it used to be. Most of my Lending Club and Prosper accounts are fully seasoned now, having gone through more than one complete cycle as loans I invested in three or even five years ago are fully repaid. I think the new normal for serious P2P lending investors is 8-10% returns rather than the 10-12% returns we have enjoyed for several years.

At the end of every quarterly update I like to highlight one number: Net Interest earned. This is the money that shows the actual gains in your account (before taxes). I always like to see this number grow because eventually, when I retire some day, I want to live off the interest generated by these investments. As I continue to add to my investments I expect this number to keep growing – it was at a record $45,935 for the year ending March 31, 2014.

Let me know what you think. I am always happy to discuss these numbers with you.