[Editor’s note: This is the first in a two part series on bitcoin P2P lending by Stu Lustman of p2plendingexpert.com. Stu is a lifer in finance who has spent the last 10 years doing credit analysis and structuring transactions in the equipment finance industry. Almost 2 years ago, he started his blog on marketplace/peer to peer lending to share how a commercial credit professional would look at and analyze these loans. For the last 6 months, his loans have included lending in Bitcoin as well across 3 different platforms.]

Bitcoin lending is something new in the world of marketplace lending. It is a complicated and confusing topic for a couple of reasons. Bitcoin is something that many people have heard of but not many understand. First of all, there are 2 Bitcoins really: Bitcoin the technology and Bitcoin the currency/payment system. The primary focus of this article is Bitcoin the currency/payment system and how marketplace lending/peer to peer lending is emerging in this currency.

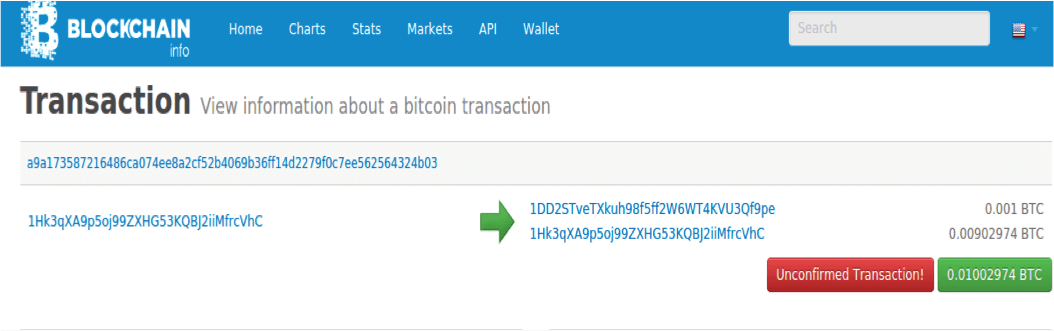

Before we get to that, we need to understand a little bit about Bitcoin (BTC) the technology. BTC is based on a ‘trustless’ decentralized public ledger called the Block Chain. The Block Chain is considered trustless because each transaction on it is confirmed numerous times by independent third parties, none of which are directly involved in the transaction they are confirming. So think of a credit card transaction where the merchant gets a confirmation from Visa and allows you to purchase your goods from their store. Now, imagine that Visa isn’t one network or bank, but it is many little distributed unrelated networks that do the confirming. That is the Block Chain. Here is a screenshot of what the Block Chain looks like (click the image below to see it at full size):

Every transaction done in BTC shows up here at Blockchain.info. What is important to note, and you can see it on this transaction, is that BTC is pseudo-anonymous. It is not totally anonymous as the sending address, which you see begins with 1HK3q is a specific identifier to a specific person and account. However, it’s not public in the way that it shows that Jimmy sent .001 BTC to Cindy. Instead address 1HK3q sent .001 BTC to 1DD2ST. This is an important feature of Bitcoin that we need to remember when we look at how to lend BTC for profit as well as how the lending platforms operate.

It is these features and Bitcoin’s use as a payment system that explain why we don’t measure how good of an investment it is. The investment potential and this article by Quartz in particular is something that Peter asked me to comment on for this post. The Quartz article looks at it differently calling it the worst investment of 2014. This article looks at Bitcoin from the viewpoint of any investment or currency. While the Quartz article does acknowledge that we enthusiasts don’t really care about price, those looking to build BTC based businesses have no more interest in its price against the dollar than a USD based business that serves its local community cares about the price of the Euro or the Ruble. It’s just a number. For me personally, I hope I never have to cash my BTC in for any other currency. The article does make concessions that many value the technology and potential payment system mentioned above as part of the 2 Bitcoins. What is important and what we do care about is price stability and despite the decline in price in 2014, we have much greater price stability and less volatility in its price. This is vitally important to increasing BTC’s reach and more widespread merchant adoption of it as a form of payment.

The idea that money gets its power from the government to consider it legal tender, as Quartz says, is to not understand what money is. Money is a store of value and a medium of exchange. It has to have both characteristics. Bitcoin is already a medium of exchange. Legal tender doesn’t make it a store of value. After all, compare what new car prices are today versus 10 years ago. The dollar is legal tender but steadily losing value each year in terms of what it buys. Price stability for BTC will help people to believe it is a store of value as well and make it an alternative form of money.

Now, back to lending in Bitcoin.

What’s different about BTC lending versus USD lending?

- Double blind versus Double Sighted

We know who our borrower is and we can interact with them directly.

- Cheap Cross border lending & Geographical Diversification

One of the biggest advantages of BTC generally, and BTC lending in particular is how cheap it is to do all financial transactions but especially cross border transactions for the equivalent of a few cents. We aren’t limited to Americans and USD. We can lend to anyone we want. I think I have more Australian borrowers I lend to than any other country including the US.

- No Credit Scores

Why we must engage with our borrowers.

- Varying loan purposes

Rates are higher so debt consolidation is less likely than the standard Prosper or Lending Club loan.

- Currency Diversification

This difference seems pretty obvious since we are lending in Bitcoin and being repaid in Bitcoin. Some platforms let you lock in a BTC/USD rate and others have it as an option and others don’t.

However, not all of the differences are benefits.

- The Wild West

The USD peer lending world has established companies, great infrastructure and great stability. The BTC lending world is so new that it has none of these things yet. It is truly the wild wild west. - Pseudo-Anonymity

Like I mentioned above, it’s important to understand this. - Much Higher Default Rates

There is a much higher likelihood, even with good diversification, that you can lose money lending out your coin. Default rates are high based on some of these reasons we have discussed already like the Wild West nature of the infrastructure and the ease of running and hiding the coin behind these complex wallet addresses.

I have been fortunate to make money and I outline my BTC loan returns on my blog p2plendingexpert.com each month but many people barely break even or lose money. Done correctly, it can really boost your overall peer lending returns.

In the second part of this series we will take a look at the three major BTC p2p lending platforms.