The Financial Health Network released its 10th annual Spend Report, showing the first-ever overall decline in spending on interest and fees.

The study follows what U.S. households spent on financial services during the pandemic and argues the 4% decline in debt spending came from the student loan debt moratorium, government stimulus, and a pandemic-related drop in credit card debt.

Still, analysts said underserved populations pay a more significant proportion of fees, and spending will likely rise as pandemic pressures ease this year.

“The last two years of the pandemic have been a roller-coaster for people financially, often forcing them to both recalibrate their lives and their finances with every new COVID development,” Financial Health Network CEO Jennifer Tescher said.

“While we’ve witnessed a rare drop in overall spending on financial services in 2021, the confluence of increased consumer spending, the end of government aid, and rising inflation all point to an increase in fees and interest for 2022; that will likely fall disproportionately on households that are already struggling financially.”

Decline in spending won’t last

Analysis of year-over-year trends for more than two-dozen financial products and services found a rare decline in overall spending. However, an outsized cost burden remains for underserved populations causing concern with an anticipated increase for the year ahead.

Total interest and fees declined 4% to $305 billion from a high of $319 billion in 2020, primarily driven by changes in spending on credit cards and student loans. This year’s report found that households considered “not financially healthy” accounted for 83% of all fees and interest paid:

| Product | Total Fees in B 2020 | Total in B 2021 | % change |

|---|---|---|---|

| Account maint. fees | $5.0 | $4.8 | -4% |

| ATM fees | $2.0 | $2.3 | +15% |

| Check cashing, nonbank | $1.6 | $1.5 | -3% |

| International remittances | $8.5 | $8.9 | +5% |

| Money orders | $0.9 | $0.9 | +2% |

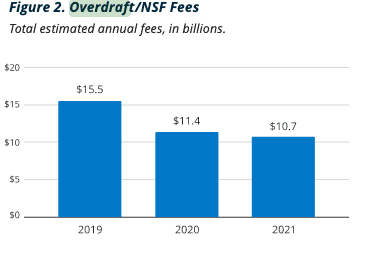

| Overdraft/NSF | $11.4 | $10.7 | -6% |

| Prepaid cards | $6.2 | $7.2 | +17% |

| TOTAL | $35.4 | $36.4 | +3% |

Despite declines in overall spending, households with lower advantages continued to trend toward higher-cost borrowing and serviced higher-cost interest.

Broken down by income, race, and ethnicity, disparities become apparent. As a percentage of their income, Black households, on average, spent 7% on fees, twice what White households spent on interest 3%, while Latinx families spent 5% or 40% more than White households.

Households with low-to-moderate incomes spent 8% of their income on fees and interest, more than twice the higher income brackets that paid 3%.

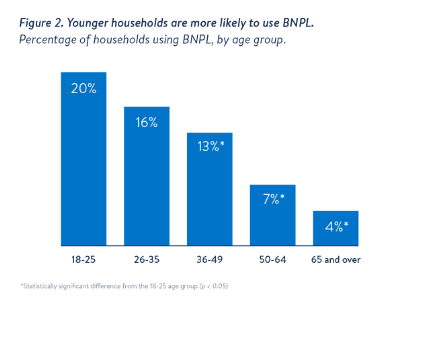

Spending differed by type of product: BNPL

After the BNPL rush that began in August, Financial Health Network saw a significant rise in the BNPL market. By March 2022, consumers paid an estimated $1 billion in total interest to popular pay-in-four or other BNPL options.

Comparatively, they estimated households carry total balances of $95 billion in interest and fees on cards in 2021.

Financial Health Network found users of BNPL are disproportionately those that struggle with their financial health.

Based on their March BNPL specific brief, one in four users of BNPL were financially vulnerable. Financial Health Network Score describes vulnerable populations as struggling with most or all aspects of their financial lives: nearly a quarter report struggling to make payments.

The study also found younger generations, like Gen Z, were looking for tech-friendly alternatives to credit cards: 20% of 18-25-year-olds surveyed reported they had used BNPL in the last 12 months.

Overdraft

Overdraft and nonsufficient funds fees appear to have leveled out, totaling roughly $11 billion in 2020 and 2021. Analysts’ recent announcements of overdraft reform by several significant banks could create positive shifts in this market in 2022.

Bank of America, for example, announced they would drop their fee to $10 on May 1. Chase dropped their fee to $34, just barely below Wells Fargo and TD Bank’s $35 fees and PNC’s $36 fee.

Meanwhile, many digital banks have dropped fees altogether, like Ally, Axos, Chime, Monzo, and Revolut.

The Financial Health Network found Black households with bank accounts were almost twice as likely as White households to report having paid at least one overdraft fee, while Latinx households were 1.5x more likely.

Financially vulnerable households with bank accounts were roughly 10-times more likely to pay overdraft fees.

Bad news: Credit card debt is back

The pandemic was heralded as a dramatic shift in U.S. credit card debt, and the trend continued throughout 2021 until the last quarter, when payback saw a record jump.

The WSJ found from the lockdown in February 2020 to June of that year that, credit debt fell 10% in the U.S .as customers stayed inside and saved.

Debt relief, pandemic stimulus, and deferred mortgage and student loans went right into paying off credit cards, declining in 2021 by 10%, but only for a while. The final quarter surprise posted a red flag for financial health, Financial Health Network said, and it approached pre-pandemic levels.

Based on New York Fed Center For Macroeconomic Data released in February 2022, it was the most significant increase in aggregate household debt since 2007.

“Aggregate limits on credit cards stepped up by $96 billion in Q4, and aggregate credit limits are now $160 billion above the pre-pandemic level,” the Fed study found. “Aggregate limits on credit card accounts now stand at $4.06 trillion, compared to $3.93 trillion in the first quarter of 2020,”

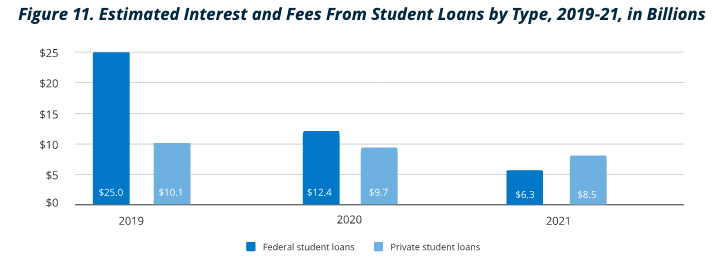

Student loans

Interest and fees on federal student loan totals fell precipitously from an estimated $25 billion in 2019 to $6.3 billion in 2021 due to the moratorium in March 2020. Unfortunately for student borrowers, the suspension ends on Aug. 31, 2022.

For every month that the moratorium is extended, the study estimates that federal student loan borrowers avoid $1.5 billion in interest payments. Federal student loans comprise 92% of the $1.7 trillion total; private student loan borrowers paid 30% more interest and fees in 2021 than federal student loan borrowers.

The good news: Pawn, payday, and title loans dropped

Financial Health Network found interest and fees for alternative financial services dropped dramatically between 2019 and 2021: pawn revenue fell 25%, payday dropped 45%, and title loans sank nearly 40%.

Payday loans, in particular, saw significant declines over the past year, with the percentage of households reporting usage dropping from 5% in 2020 to 3% in 2021.

Black households, households with low to moderate incomes, and financially vulnerable households all reported significant drops in the usage of payday loans.

“One of the reasons we collaborate with the Financial Health Network is to further evaluate how households managed their finances through the pandemic,” Sarah Keh, VP of Inclusive Solutions at Prudential, said.

“Access to high-quality, affordable financial services — especially across race, ethnicity, and income — provides data for researchers, policymakers and advocates to track trends and identify opportunities to support more equitable financial health policies and products.”

Year in review

As 2021 came to a close, spending on several products returned to the pre-pandemic mean. Credit card balances fell dramatically but rebounded right in time for holiday spending. Balances on installment loans also grew in the second half of 2021, as did overdraft fees.

The report found that; “If household spending continues to grow, interest rates increase as expected, and the remaining government supports end as projected, we anticipate that 2022 will increase overall interest and fees on financial services. Households struggling financially will likely feel these impacts most acutely.”

Methodology

It’s the decennial of the spend report but the second under a new methodology that matches research with a nationally representative survey on consumer spending. The survey of more than 5,000 U.S.-based adults went out in November 2021.

In closing, the Financial Health Network said in 2022, it will work on briefs that “take closer looks at products with particular implications for policymakers, financial service providers, and financial health in general.”