What do you get if you take decades of experience in the automobile and finance industries and merge it with a quality machine learning model?

In Steve Burke’s case, you get Agora Data, a company that helps any size of auto dealer compete with the big corporations by providing affordable financing at more reasonable rates.

Burke began his career in the car business in the late 1970s. He quickly learned how hard it was to raise the capital he needed to meet growth goals. From there, he worked in indirect auto finance, buying non-prime loans from dealers and other originators.

In finance, capital was available in abundance. Why couldn’t it be like that for auto finance? In 2016 Burke and two of his sons created a platform designed to connect the average car dealer to capital markets.

The importance of standardized data in Agora Data’s models

At the onset, Burke had data on $8 billion in non-prime loans from origination to liquidation. He fed that into his model to start Agora Marketplace, a service introducing buyers and sellers of loans.

Key to its success was the model’s ability to standardize data from different formats, Burke explained. In 2017 it integrated with 10 other systems to allow the push of native data directly from the dealer. That capability quickly grew the size of Agora’s data pool to $12 billion.

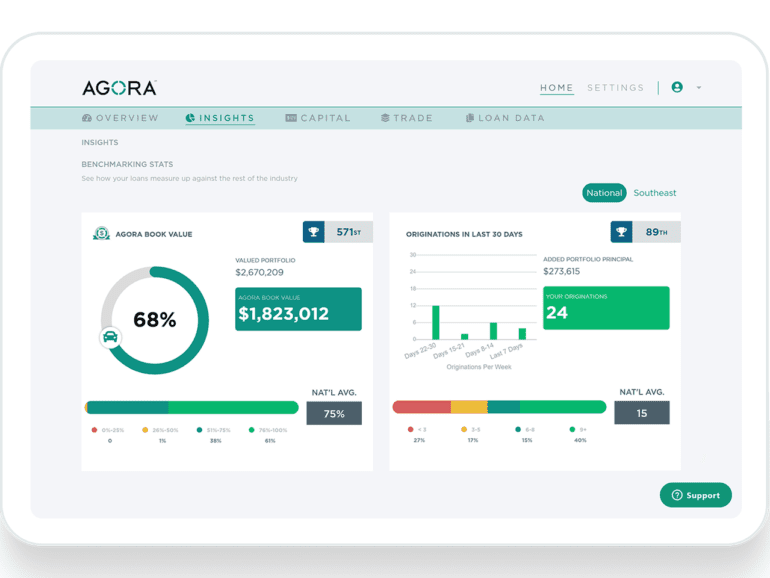

That large data pool led, in 2018, to the debut of Agora Insights, a service that provides car dealers with detailed knowledge of their market and portfolios.

“You can benchmark against other dealers in your town, region, state, and nationally and get some good insights into how you’re doing business and how others do business,” Burke said.

Burke then developed a tool that allowed dealers to negotiate from positions of strength. Agora Book Value provides on-demand book values for loans. Believed to be the first of its kind, Agora Book Value helps educate dealers on what their loans are worth in the marketplace, so they can get actual value instead of taking somebody’s word for it. Burke said it provides 98% accuracy on portfolios worth at least $4.5 million.

How Agora Data created the first crowdsourced auto loan securitization

Like pioneering fintech across sectors, Burke offered value to customers because they provided him significant value in return.

“We gave those valuable insights to car dealers, and the trade was we would receive data,” Burke explained. “We don’t charge anything that was our freemium part of our platform. That was to enable dealers to push data to us. They got back some precious information in return.

The innovation continued when Agora facilitated what Burke said is the world’s first crowdsourced subprime auto securitization in late 2020. Before that, the average car dealer didn’t have the scale of a GMAC to contemplate a securitization.

The technology aggregated dealers’ balance sheets, LTVs, and APRs into one deal. Agora Data has completed four such securitizations so far.

Why crowdsourced auto loan securitizations are hard to do

Why has it taken so long for someone to do it? The short answer is because it is hard, Burke said. Securitizing one company’s assets are complex, never mind those across multiple asset classes. While predicting losses on prime loans is easier, non-prime tools do not accurately predict failure.

The second reason is that it is an expensive process, Burke said. The tabs run into many millions of dollars between legal, structuring, and modeling costs.

“We’ve been able to take what isn’t a very predictable asset class of non-prime loans and make it as predictable, if not more predictable than a prime one,” he said. “I think that separates us from the rest of the pack.”

While Burke doesn’t discount the possibility of applying Agora Data’s technology beyond auto loans, he said there is plenty of opportunity within it to keep the team busy for some time. It’s a $1.5 trillion market. When you boil down any consumer loan, the components are similar.

Market factors are conducive to continued growth

Agora Data is well-positioned for any coming market turbulence, Burke believes. During the recession that started in 2008, non-prime auto loans thrived. Fast-forward to the pandemic and the recession we may or may not be in.

The stimulus has artificially inflated disposable income levels, creating high vehicle demand. Delinquencies and charge rates fell, as a result, leaving defaults well below pre-pandemic levels. Burke hasn’t seen the level of damage predicted by the New York Fed. While defaults have risen, they are still low.

Burke is confident that Agora Data’s macro and micro models will maintain accuracy.

Used car prices are inflated, so more people will fall underwater when they eventually drop. That will affect non-prime borrowers the most. Until then, the market will maintain health because repos generate higher recovery amounts, leaving less to write off.

“Even if repossession rates slightly increase, I still think the cumulative net loss will be below pre-pandemic levels for quite some time,” Burke concluded.